Public Assets - Key to Meet Fiscal Challenges

…But International Guidelines Need Updating

By Ian Ball and Dag Detter, January 7, 2025

Ian Ball is one of the principal architects of the New Zealand government’s financial management reforms. He was Chief Executive Officer of the International Federation of Accountants (IFAC).

From 1998 - 2001, Dag Detter Led A Restructuring of The $70 Billion Portfolio of Swedish Government-Owned Companies, The First Attempt By A European Government to Address Systematically The Ownership & Management Of Government Enterprises & Real Estate.

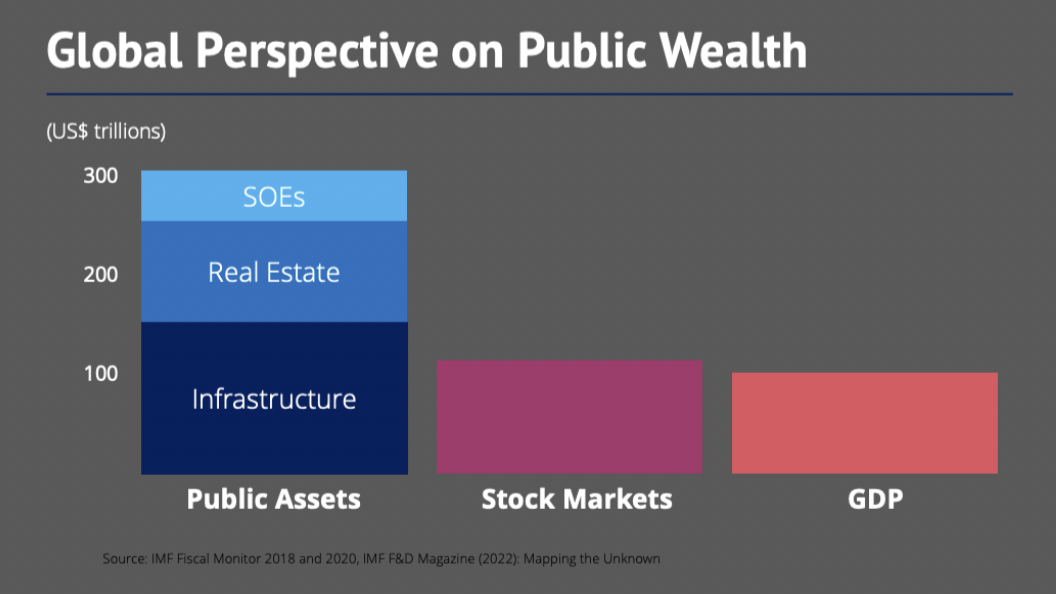

Governments worldwide own more assets than ever before. The total value is larger than all global capital markets combined. Most likely, it is equivalent to three times the global GDP, according to estimates from the IMF. Half of this, or one and a half times GDP, are commercial assets such as real estate and government-owned corporations. But unlike listed equity assets, public wealth is largely unaudited, unsupervised, and often unregulated. Even worse, it is almost entirely unaccounted for. When developing their budgets, most governments largely ignore the assets they own and the value those assets could generate.

After the 1980s recession, governments focused on selling commercial assets in the hope that this would improve their efficiency and productivity, generate cash for much-needed capital expenditures, remove the related debt from the government balance sheet, and avoid a conflict with public sector borrowing targets.

This recipe became part of the standard reform package promoted for crisis-wracked countries by Washington, D.C.-based institutions such as the IMF, World Bank and US Treasury.

Contrary to the trend of selling off public commercial assets, Sweden became the first developed economy to actively manage its portfolio of assets “as if privately owned.” At the end of the ‘90s, the Swedish government portfolio was the most extensive corporate portfolio in the country, representing a quarter of the domestic business sector. This vast portfolio of loss-making state-owned companies contributed to the outsized public expenses, hiding the size of unemployment and public debt.

Following Sweden’s successful transformation, the OECD Guidelines on Corporate Governance of State-Owned Enterprises (SOEs) were developed. These guidelines recommend more transparency and the consolidated management of SOEs in an independent, professionally managed vehicle at arms’ length from short-term political interference. Since then, the OECD Guidelines have been the norm among international institutions regarding the management of public commercial assets. Twenty-five years ago, they were undoubtedly a good initiative. An update is now urgently required..

As with a medical emergency, if you have an injured leg, we can’t just rely on that better ‘transparency’’: an X-ray and an ‘independent vehicle’; a separate room would immediately put you back on your feet. We expect an integrated process to bring you back to your previous level of physical activity. This would include a specialist doctor to interpret the X-ray images, another specialist to diagnose and remedy, and finally, a physiotherapist for rehabilitation to a full recovery.

Professionally managed, public assets can generate non-tax revenues, providing much-needed fiscal space and improve debt sustainability. However, this requires a financial perspective and purpose to govern the portfolio and individual companies. Just publishing financial statements several months after the year-end as a token of proper transparency will not help.

Institutionalising an accrual-based financial management system in the government and the public sector would improve all stakeholders’ understanding of the value of public sector assets and liabilities. It would also enhance their comprehension of how more efficiently managed assets could improve net worth and productivity, generating dividends for the government budget.

New Zealand pioneered accrual-based and balance sheet-oriented public financial management in the late 1980s, switching away from the cash-based systems traditionally used by governments. This forced departments to think long-term and significantly increase the efficiency of their asset use. It helped bring New Zealand away from the brink of economic collapse. Since then, the fiscal position has steadily improved, with the government increasing or maintaining its net worth virtually every year in the past 30 years except immediately following the global financial crisis, the earthquakes and the pandemic.

The benefits to a country from having a strong balance sheet are very much like those to an individual. There is a greater ability to absorb shocks or surprises without being forced to take drastic remedial steps – you can fix the car without having to cut the food budget. This was demonstrated in how the government bounced back financially from the financial crisis, the earthquakes, and Covid-19.

A strong balance sheet also enables easier access to emergency debt financing, which may be part of managing a shock. Coupled with this is the benefit of being able to borrow more easily and cheaply in normal times if necessary or desirable. This might be useful, for example, if there is a need to invest in infrastructure.

Given the current fiscal challenges faced by governments, including climate, demography, and geopolitics, they urgently need to manage SOEs and other public assets in a manner that recognizes the contribution they can make to balance sheet strength. The OECD Guidelines should be updated to reflect this, and governments should change their fiscal focus from debt to the whole balance sheet, with net worth as the summary measure. International institutions such as the IMF and the World Bank explicitly recognise the importance of better management of government balance sheets, and for many countries, the IFIs will be critical in supporting governments in making the necessary transition.

Through better asset and liability management, government revenues can be increased significantly – by several per cent of GDP per annum in the estimation of the IMF. Professional management of public commercial assets would also increase private and public sector investments, boost capital markets, diversify and grow the economy. All desperately needed across the world.

The time is now for governments to properly use the hidden goldmine of public assets to meet their fiscal challenges. This should also be a priority for the IFIs in supporting countries seeking to implement these changes.

——————